Spring planting season is here and American farmers face fertilizer shock due to a crisis in the Persian Gulf, more than 7,000 miles away. Following joint U.S.-Israeli strikes on Iran on February 28, 2026, the Strait of Hormuz has effectively closed, creating a chokepoint in global oil, natural gas, and fertilizer trade 1. The timing of the closure is particularly problematic for U.S. crop producers because the spring planting season sees the largest volumes of fertilizer imports on average 12. And given it takes 30 days for vessels from the Persian Gulf to the U.S. Gulf Coast, fertilizer disruptions will hit peak planting period in March and April 1. The Fertilizer Institute forecasts that U.S. farmers will face a limited supply of about 2 million tons of urea this spring, where prices have already spiked close to 30% 3.

The Strait of Hormuz matters for global agriculture as it supports 20–30% of global fertilizer exports, including 35% of global urea exports 1. About half the world’s sulfur exports, a key ingredient for phosphate fertilizer, are also shipped through the Strait 3. There is not much hope for large alternative suppliers as well because Russia faces domestic export limits due to domestic demand for fertilizers, and China may extend its 2021 phosphate export restrictions to protect domestic markets 1.

Quantifying U.S. crop industry’s structural vulnerability

While fertilizer import is the obvious pressure point for the U.S. crop industry, applying the input-output exposure framework in Wahdat & Lusk (2023) to the crop industry 4, I quantify the U.S. crop industry’s structural and geographic vulnerability to upstream input purchases from the pesticide/fertilizer industry. Using 2025 input-output data from Lightcast, my analysis identifies nine upstream industries to which the U.S. crop industry (NAICS 111) is “overexposed” in terms of input purchases. In other words, the crop industry is heavily reliant on these nine upstream industries for input purchases relative to a typical upstream industry. Collectively, the value of these overexposed purchases stands at $75.7 billion based on 2025 data. Three of the nine upstream industries dominate, accounting for 71.6% of that total, i.e., Crop Production (crop industry buys inputs from itself such as seeds and planting materials), Support Activities for Crop Production (NAICS 1151), and Pesticide, Fertilizer, and Other Agricultural Chemical Manufacturing (NAICS 3253).

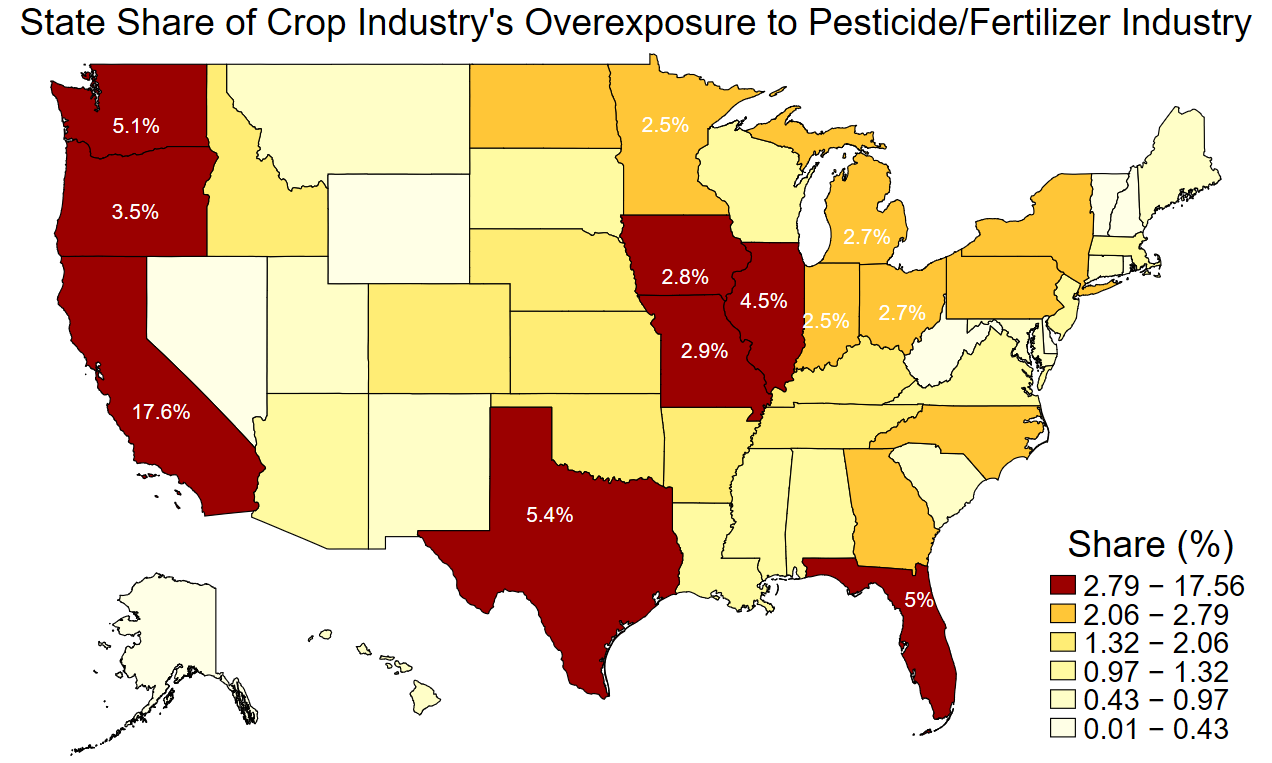

The pesticide/fertilizer industry alone represents about $13.5 billion (18%) of total overexposed upstream purchases by the U.S. crop industry, and roughly 80% of these purchases are imported by the pesticide/fertilizer industry from other US states and foreign countries. Importantly, this heavy reliance is not limited to a single state or region. The crop industry’s purchases from the pesticide/fertilizer industry are overexposed in every single U.S. state. Figure 1 displays the share of U.S. crop industry’s overexposed purchases from the pesticide/fertilizer industry by each state. It reveals how concentrated the vulnerability is across major agricultural states. California leads with over 17.6% of national overexposed purchases, followed by Texas (5.4%), Washington (5.1%), Florida (5%), and Illinois (4.5%). Major Corn Belt and surrounding states such as Iowa (2.8%), Missouri (2.9%), Michigan (2.7%), Ohio (2.7%), Indiana (2.5%), Minnesota (2.5%), Pennsylvania (2.4%), and North Carolina (2.3%) are also exposed. There isn’t a single state that will be spared by the fertilizer shock.

The cascading effects and self-reinforcements

From a food supply chain perspective, the Strait of Hormuz fertilizer shock is particularly concerning due to its chain of second-order effects. The input-output exposure framework in Wahdat & Lusk (2023) is specifically designed to trace such effects. Because the U.S. crop industry is heavily reliant on itself for upstream inputs, disruptions to the industry’s inputs will also affect its outputs. For instance, when seed quality suffers, the crop industry’s purchases from itself are also affected. An input shock cascades into a self-reinforcing production shock.

The production shock in the crop industry then extends to the animal production industry (NAICS 112). Approximately 9% of the animal production industry’s overexposed upstream purchases come from the crop industry including feed grains, forage, and other crop outputs. If crop industry’s output deteriorates in quality or price, it affects the input conditions facing livestock and poultry producers. And once again, the self-reinforcing dynamic repeats for the animal production industry, i.e., approximately 62% of the animal production industry’s own overexposed purchases are from itself such as feeder livestock and breeding stock among others. In sum, a shock to crop industry’s inputs won’t stop at the farm gate, it will ripple through itself and the animal production industry. This is the structural anatomy of the U.S. food supply chain, and it is being put to test with the Strait of Hormuz closure.

The road ahead

In the near term, policymakers should prioritize diversifying fertilizer import sources, and consider strategic reserve options for key agricultural chemicals. Reportedly, the Trump administration is lifting import barriers on fertilizers from Venezuela and Morocco 13. United States could also scale domestic production of fertilizers (think phosphate) to some extent, however, that would need key chemicals such as sulfur. In fact, half of world’s sulfur exports were shipped through the Strait of Hormuz 3.

In the long run, the structural heavy reliance identified in this analysis points to the need for more resilient domestic supply chains for pesticides, fertilizers, and chemical agricultural inputs. An industry that is overexposed to a single upstream industry, which in turn imports from a high-risk region like the Persian Gulf, is an industry that lacks geographic and structural resilience.

-

Curtis, E., Virzi, J., & Welsh, C. (2026). Chokepoint: How the war with Iran threatens global food security. Center for Strategic and International Studies (CSIS). March 11. https://www.csis.org/analysis/chokepoint-how-war-iran-threatens-global-food-security ↩ ↩2 ↩3 ↩4 ↩5 ↩6

-

Arita, S., Chakravorty, R., Kim, J., Lwin, W., & Steinbach, S. (2026). Strait of Hormuz closure and fertilizer supply risks for U.S. agriculture. farmdoc daily (16):48, University of Illinois at Urbana-Champaign. March 23. https://farmdocdaily.illinois.edu/2026/03/strait-of-hormuz-closure-and-fertilizer-supply-risks-for-us-agriculture.html ↩

-

Morris, F. (2026). War with Iran disrupts fertilizer exports as U.S. farmers prepare for planting season. NPR / KCUR. March 26. https://www.npr.org/2026/03/26/g-s1-115240/iran-war-strait-hormuz-fertilizer-exports-farmers-planting-season ↩ ↩2 ↩3 ↩4

-

Wahdat, A. Z., & Lusk, J. L. (2023). The Achilles Heel of the U.S. Food Industries: Exposure to Labor and Upstream Industries in the Supply Chain. American Journal of Agricultural Economics. https://doi.org/10.1111/ajae.12331 ↩